Pork production continues to rise (+5% over the past year) although Russia managed to achieve self-sufficiency in this type of meat a few years ago. In 2022, there was a record high consumption of pork per capita – 29.8 kg.

Despite the growth of production indicators, the year of 2022 can’t be called quiet for the pork industry. There were problems with the supply of feed additives, veterinary drugs, genetic material and equipment for swine farms. The logistical challenges, strengthening of the ruble and COVID restrictions in consumer countries limited the export supplies. Difficulties in the financial sector reduced the availability of governmental support in the form of additional preferential revolving loans and investment loans for genetic selection centres and pork slaughter and processing plants.

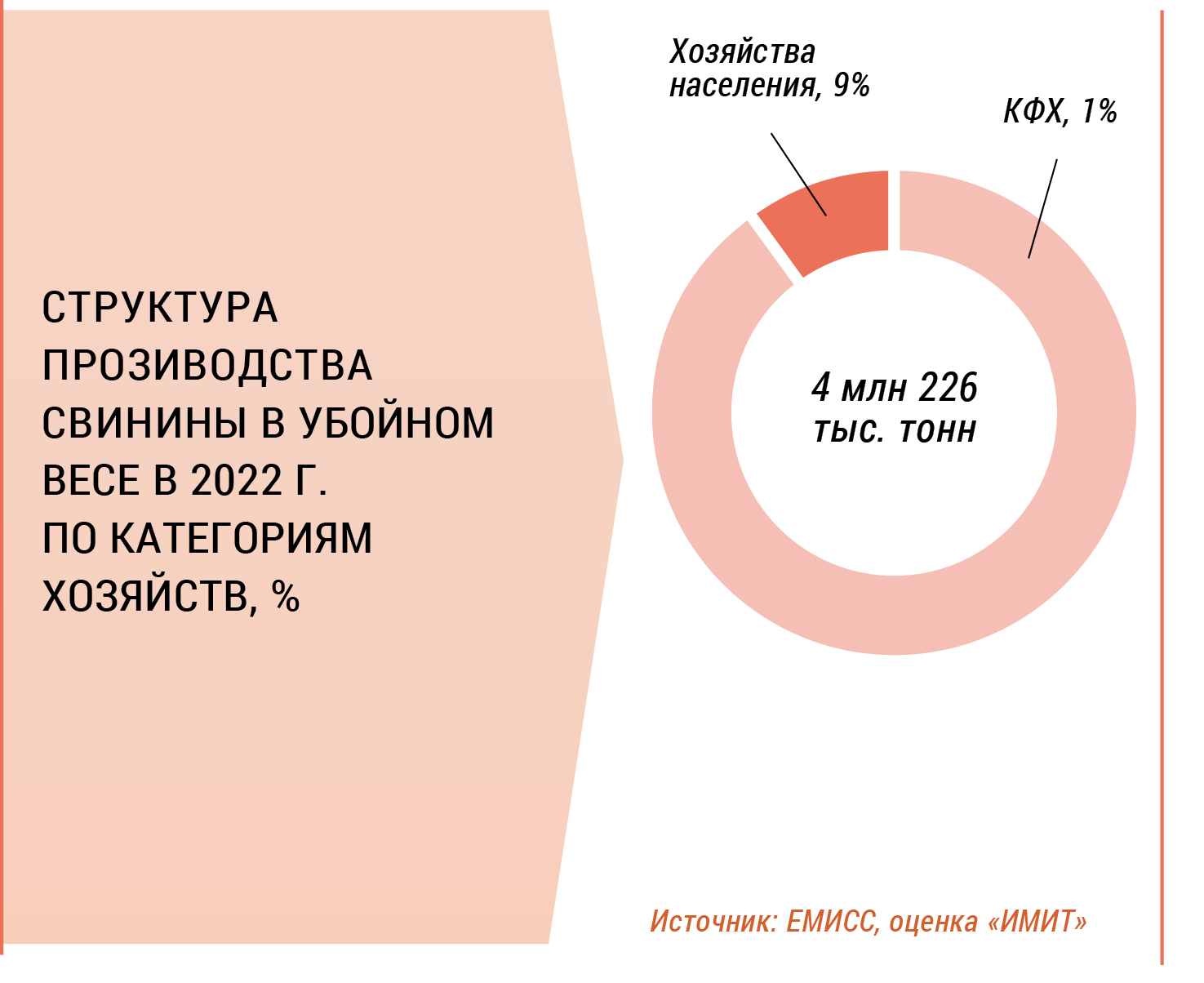

Peasant Farms Produce Less Pork

Last year, Russia produced 4,226 K tons of pork on a carcass weight basis (+248 K tons versus 2021).

In recent years, there’s a growing tendency of decreasing output by peasant and private farms, while the main volume of pork is supplied by the pork industry. The large vertically integrated holding companies are generally more competitive and resistant to economic risks. They are better able to cope with the epizootic threats (ASF).

In 2022, agricultural companies produced by 6.9% more pork (+243 K tons), namely, 3,839 K tons. Private farms decreased their output by 10.2%, peasant farms – by 14.9% compared to 2021.

Similar momentum continued at the beginning of this year. In the first month, industrial companies produced 315 K tons of pork on a carcass weight basis: compared to January, 2021, the increase was 9.6% (+227.6 K tons). The pig population in the industrial sector increased by 7% (+1.7 mln), however, it continued to decrease in households (-16.3%).

Consolidation of Assets

Last year, top 10 Russian companies accounted for 62% of the industrial pork production market volume, while 91% were produced by new modernized companies. The leader in the pork production is “Miratorg”. Its share in the total industrial production volume is about 13% (487 K tons on a carcass weight basis in 2022). “Sibagro” takes the second place with a share of 7%. This company reached top 5 in just two years by increasing its production capacity from 151 K tons in 2020 to 284 K tons in 2022. “Rusagro” takes the third place with a share of 6.4% (246 K tons).

The market experts noted that over the last three years, the growth rate in the pork industry was generally more moderate than several years ago. One of the reasons for that is the implementation of most major investment projects, the end of the governmental support programs and preferential loans in the sub-industry.

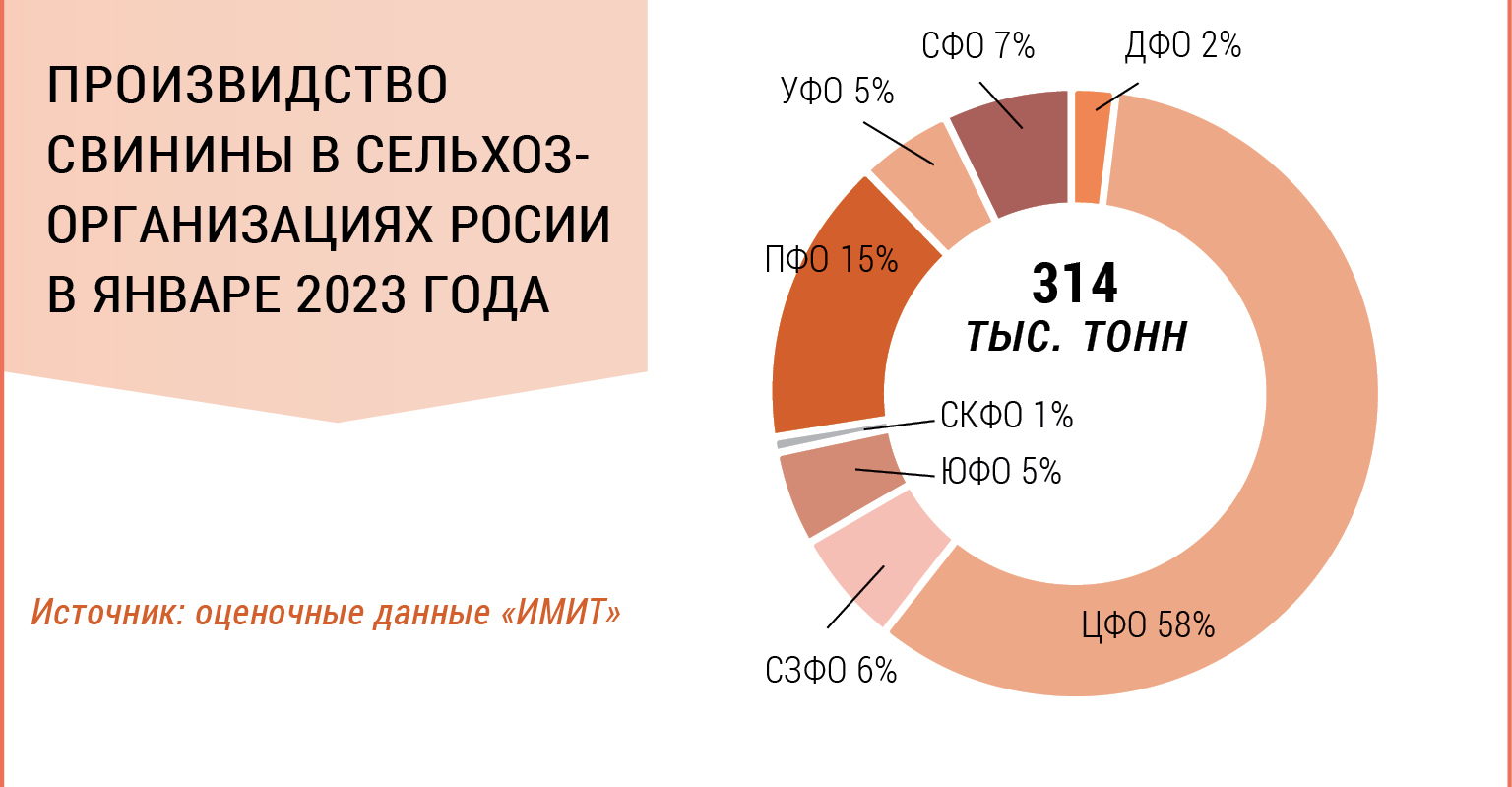

Central Federal District Leads in Production

The pork production is unevenly distributed by regions, with the Central Federal District taking the first place. In 2022, this District produced 52% (+7.9% versus 2021), namely, 2,184 K tons. These indicators increased in January 2023, reaching 58% (+12.1%).

Almost all districts showed a positive momentum in 2022, with only three districts showing a negative trend. The pork production decreased in the North-West District (-11.6%), the Southern District (-2.5%) and the North Caucasus Federal District (-1%).

The experts of “IMIT” noted that Belgorod region was the main supplier of pork: in 2022, the surplus reached 592 K tons. The surplus in the Central Federal District was 957 K tons which covered the deficit in the recipient regions: in 2022, only 20 (out of 80) regions were able to provide themselves with pork by 100%.

Price Changes

In 2022, the pork prices in the Russian market were uneven. From February to April, analysts recorded a sharp rise in the prices. For example, in March, the prices of pork sides hit a record high of 201 rubles per kg. This was due to the logistical problems in the regions bordering Ukraine, increased demand by meat processors that were buying raw meat in advance amid the unstable situation with the exchange rates and the risk of stopping meat imports.

By mid-year, the situation normalized and the price momentum became largely similar to the previous periods of time. By December, the prices of pork sides significantly dropped, and the average sale price was 167 rubles per kg, due to the increased supply.

The average prices of live pork and pork sides dropped by 5% in late 2022 versus 2021, however, the prices of clear pork and by-products increased (+7% on an annual basis).

In February this year, the price of pork sides dropped by 3.9%. In Central Federal District, the prices decreased to 153 rubles per kg (-8.6% versus January, 2023). In a year, the average market price of pork sides decreased by 4.4%.

Imports Rose, but Only in the First Half of the Year

Pork imports rose in 2022 due to the duty-free entry within the quota of 100 K tons in the first half of the year. In the 3rd and 4th quarters, however, the supply dropped sharply.

Last year, the share of pork in the meat imports reached 4% (+54% versus 2021). The overall import of pork to Russia was 18.2 K tons, which was by 6.3 K tons more than in the previous year. The main suppliers were Latin American countries: Brazil (91%), Chile (7%) and Argentina (1%), while the Republic of Belarus and Kazakhstan accounted for about 1% (“IMIT” evaluation).

The industry experts are convinced that this year the imports will not rise because the domestic production continues to increase, while the exports don’t grow, and there is an additional amount of pork going to the Russian market. This is confirmed by the most recent data: in January, the share of pork in the meat imports decreased to only 0.2% (-98% versus January, 2022).

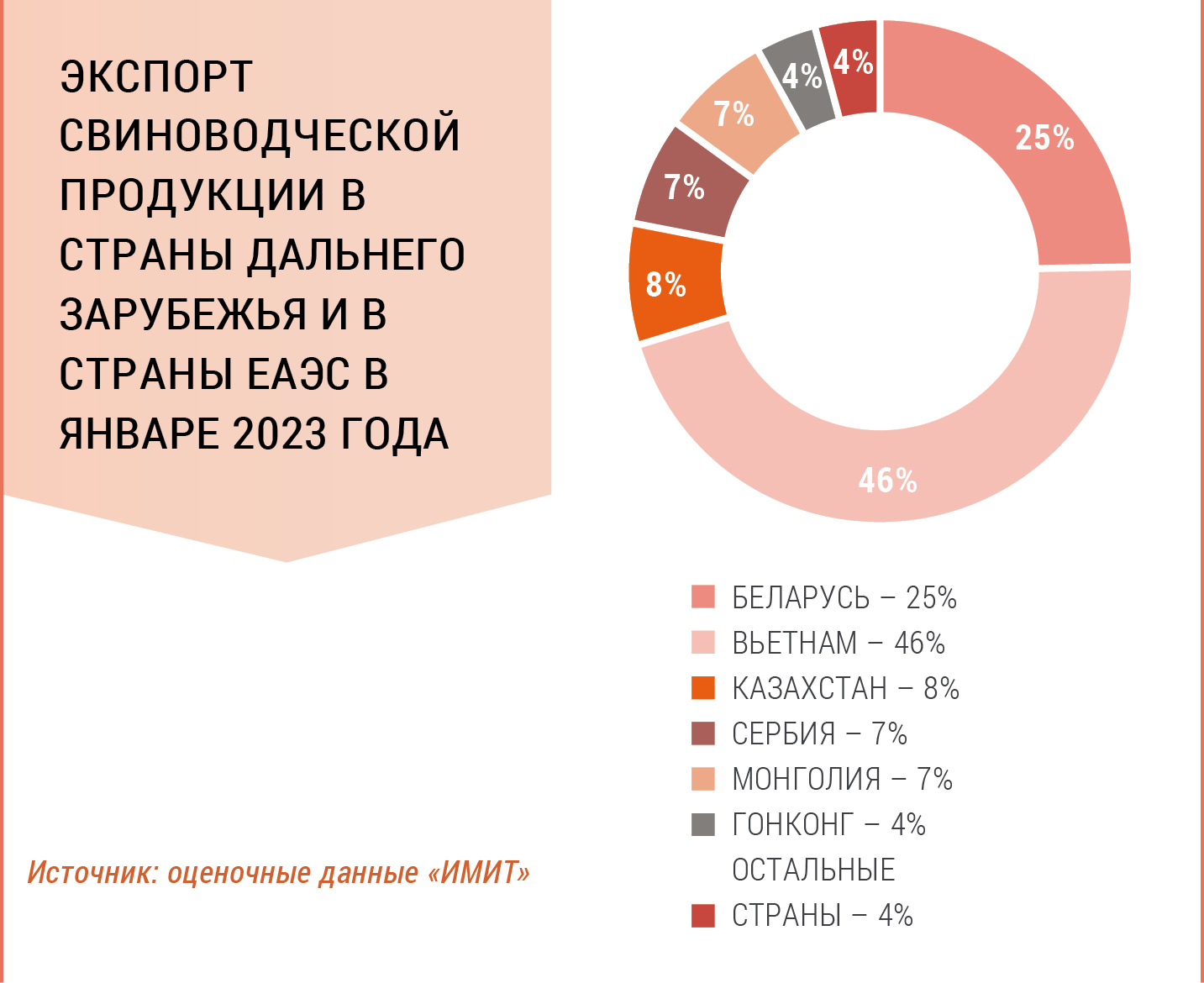

Exports Reduced by 10%

According to the “IMIT” evaluation, last year, pork export supplies dropped by 10% to 170 K tons. The amount of exported pork was by 20 K tons less than in 2021. The main reasons for that were logistical problems, deficit of containers, recovery of the importing countries’ own production (Vietnam) and strengthening of the ruble, which had a negative impact on the profitability of deliveries.

Russian pork was mainly exported to the Republic of Belarus, Vietnam and Kazakhstan, which accounted for 83% of the exports.

There was a positive momentum in January, 2023: Russia exported 14.4 K tons of pork (+77% for the year). The supplies increased by 102% in the first month of the year versus December, 2022.

Notably, the Republic of Belarus imported about 60% of Russian pork, while it was only about 30% in January, 2022. The supplies to Serbia, Vietnam, Mongolia, Hong Kong, Armenia and Kyrgyzstan significantly increased.

Forecasts and Risk Factors

Speaking of the total pork market volume, in 2022, it reached 3,701 K tons, rising by 8% during the year, while the import share was minimal (0.5%). The growth continues: according to the “IMIT” estimates, the pork market volume was 300 K tons in January, 2023, which is by 7% higher than the last January’s volume.

“The pig population in the large agricultural holding companies continues to rise,” said Lubov Savkina, CEO of “IMIT”. “Due to the production rise, the supply is also increasing, which means that the wholesale prices will drop this year.”

The expert also added that the grain price reduction in the second half of last year had a positive effect on the pork industry profitability.

“Speaking of the industry risks, the most important ones are the growing competition, the fight for consumers in the domestic market: this competition will mostly affect the quality and prices of the products. These factors can keep consumers hooked in 2023, and maybe attract new consumers, increase the demand and average per capita consumption, if the market is provided with high quality, not injected, pork at a price affordable by purchasers. At the same time, however, the rising prices or lower quality of meat expose companies to the risk of losing consumers,” Lubov Savkina also added.

Author: Ekaterina Broun, information and analytical agency “IMIT”.